Resilience Over Efficiency: How Geopolitical Risk Is Redrawing Asia's Digital Infrastructure Map

As subsea cable investment accelerates across Asia-Pacific, the logic driving it has fundamentally shifted. Understanding that shift, and what it demands of investors and governments, is now a strategic imperative.

For three decades, digital infrastructure was built around a single principle: efficiency. That assumption is no longer operative. What is replacing it — quietly, deliberately, and with significant capital behind it, is resilience.

The Assumption That Built the Internet

For three decades, digital infrastructure was designed around a single dominant principle: efficiency.

The shortest route. The lowest latency. The fastest connection between two points of economic gravity. Cables followed trade flows. Consortiums formed around commercial logic. Routing decisions were engineering problems, not political ones.

That assumption is no longer operative.

What is replacing it, quietly, deliberately, and with significant capital behind it, is resilience: the capacity to absorb disruption, reroute around failure, and maintain function when a node, a chokepoint, or a relationship is removed from the equation.

This is not a marginal adjustment to infrastructure planning. It is a structural reorientation, and its implications extend well beyond the technology sector.

The Fracture Lines Beneath the Surface

The catalyst is well understood in broad terms: the deepening strategic competition between the United States and China, and the ripple effects it is producing across supply chains, technology ecosystems, and now physical infrastructure.

What is less well understood is how comprehensively this competition has migrated beneath the ocean.

Approximately 99 percent of international data traffic travels via subsea cable. These cables carry financial transactions, government communications, cloud services, and the data flows that underpin modern commerce. For most of their history, they were treated as neutral infrastructure: commercially operated, internationally shared, and largely invisible to geopolitical analysis.

That neutrality is eroding.

US restrictions on Huawei Marine Networks have effectively bifurcated the global cable industry along geopolitical lines. Washington's Clean Network Initiative and subsequent technology security frameworks have introduced nationality considerations into decisions that were once purely technical. The Federal Communications Commission now reviews international cable landing licences with a scrutiny that would have been unrecognisable a decade ago.

Meanwhile, the South China Sea, through which a significant share of Asia-Pacific submarine cable traffic passes, has become an arena of strategic contestation with direct implications for infrastructure security. The SJC2 cable, connecting Singapore, Thailand, Vietnam, and Japan, was delayed for years after Beijing's permit demands for construction in waters it claims forced a costly reroute through the Philippines and Indonesia. The risk, in other words, is not hypothetical. Cable cuts in the Red Sea in 2024, linked to Houthi activity, demonstrated how quickly physical disruption to submarine infrastructure can produce cascading effects on regional connectivity.

The efficiency model assumed stable geopolitics. Stable geopolitics no longer exists.

The Rise of Alternative Digital Pathways

Across Asia-Pacific, the response to this new reality is materialising in the form of new subsea cable investments and consortiums, structured not simply to expand capacity, but to deliberately diversify routes and reduce geopolitical exposure.

Thailand is increasingly central to this emerging network. The pattern of investment is instructive, and the strategic logic running through each project deserves to be read carefully.

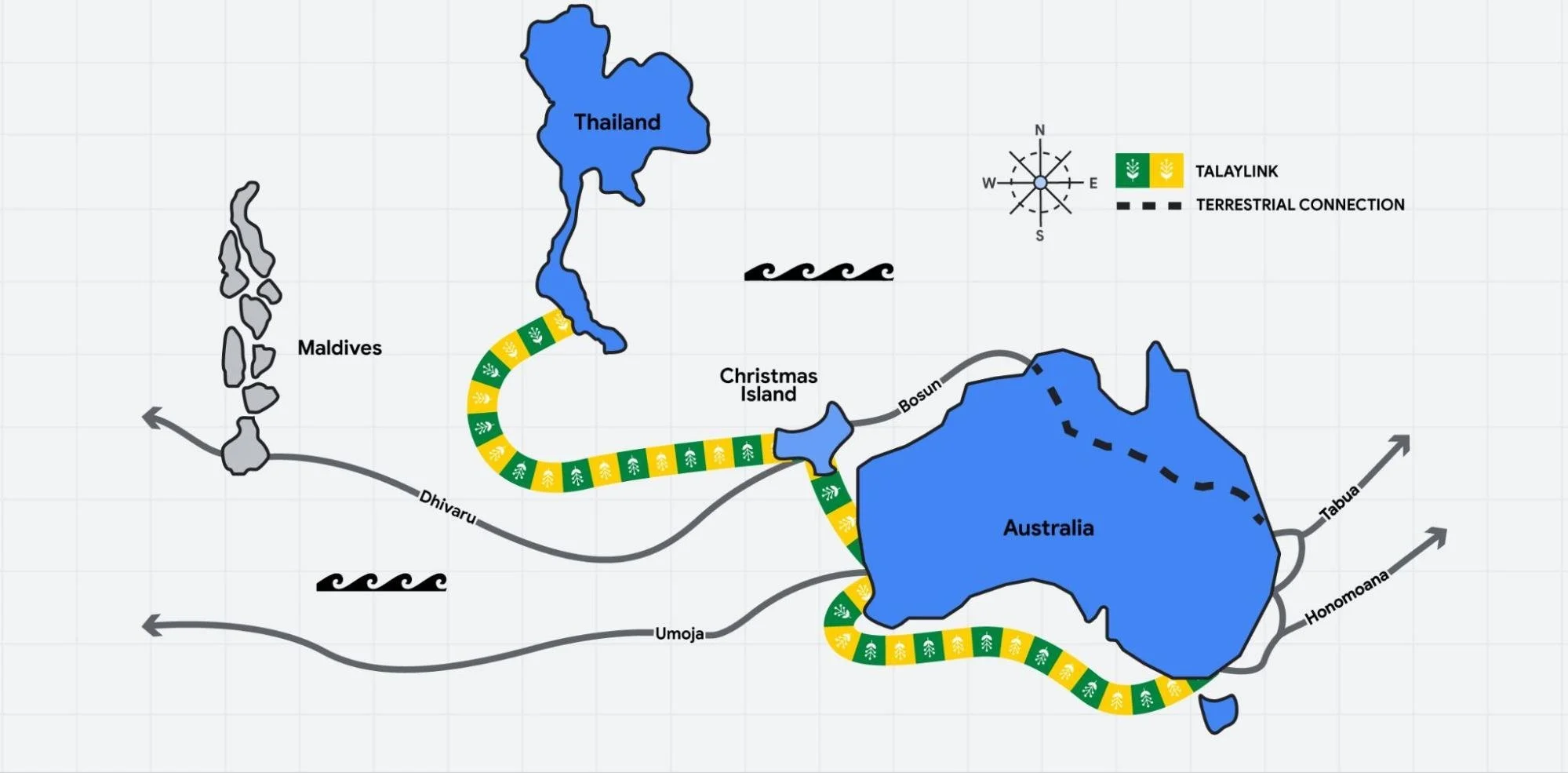

TalayLink - announced November 2025, completion date not yet disclosed

Led by Google Cloud under its Australia Connect initiative, TalayLink establishes a direct Australia–Thailand corridor via the Indian Ocean, routing west of the Sunda Strait and deliberately bypassing the more congested and contested routes that carry the majority of existing traffic. Partners include AIS for colocation and IGC, a subsidiary of ALT Telecom, as the cable landing operator. The announcement was endorsed by the Thailand Board of Investment, which positioned it explicitly within Thailand's national AI and digital economy strategy. The routing choice is not incidental: it reflects a conscious decision to create geographic separation from South China Sea exposure.

The investment logic behind TalayLink connects directly to Thailand's broader emergence as a regional data centre hub, driven by cloud expansion and AI infrastructure demand. We examined that story separately here.

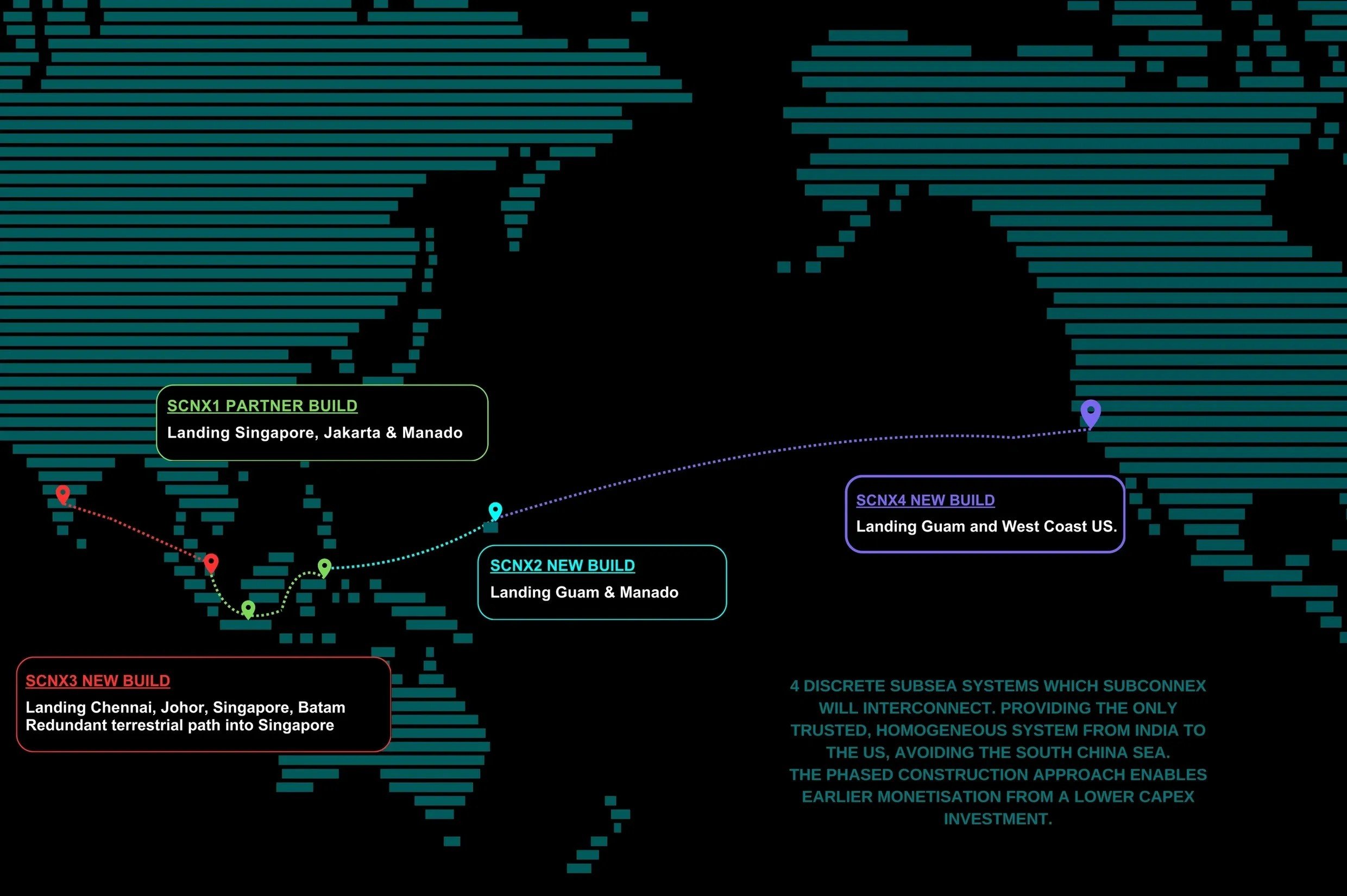

SCNX-3 - under feasibility study

Backed by a USTDA grant and developed by SubConnex with US-based APTelecom as study partner, SCNX-3 is exploring a primary route connecting Chennai (India) with Singapore, with Thailand among the potential additional landing points. At first reading, it is an infrastructure feasibility exercise. In reality, it is something more pointed: a US government-backed effort to build a "trusted" cable corridor across a region where the definition of trusted infrastructure has become a live political question. The word trusted carries deliberate geopolitical weight.

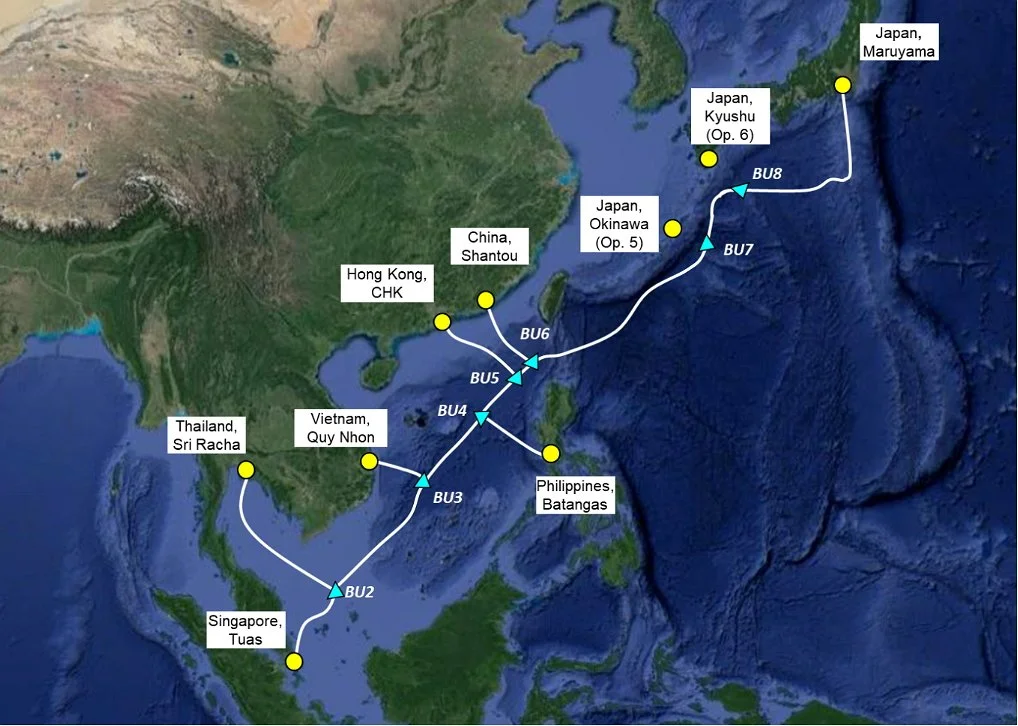

Asia Direct Cable (ADC) - operational since November 2024

A nearly 10,000km system developed by a multinational consortium including National Telecom (NT), Thailand's state-owned operator formed by the merger of CAT and TOT, ADC connects Thailand with Singapore, Vietnam, the Philippines, Japan, Hong Kong, and China. Completed by NEC and formally inaugurated in December 2024, ADC is notable for the composition of its consortium, which includes Chinese operators alongside regional and Japanese partners. This reflects the continued commercial reality that cable infrastructure has not fully decoupled along geopolitical lines.

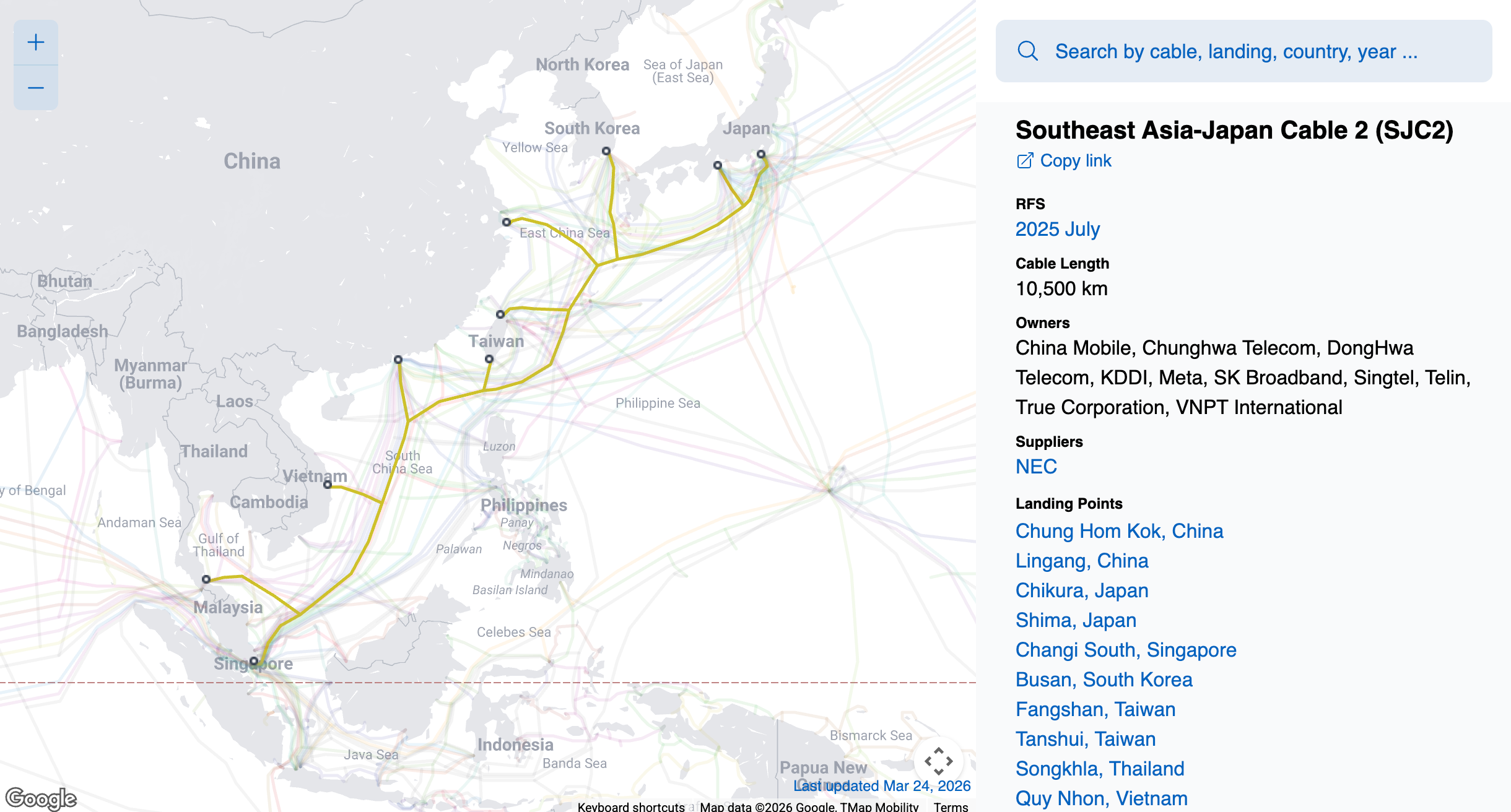

Southeast Asia–Japan Cable 2 (SJC2) - operational since July 2025

A 10,500km system in which True Internet Corporation, a subsidiary of Thailand's TRUE Group, participates as a consortium member, SJC2 connects Thailand with Japan, Singapore, Hong Kong, South Korea, and Vietnam. Its journey to operation is itself a case study in geopolitical risk: the cable entered service in 2025, years behind its original schedule, after protracted permitting delays caused by Beijing's objections to construction in waters it claims under the nine-dash line. The eventual rerouting through the Philippines and Indonesia added cost, time, and complexity. It is a preview of what infrastructure investors in this region can expect.

Individually, these are infrastructure investments. Collectively, they represent a deliberate diversification of Asia's digital backbone and Thailand's emergence as a node of strategic connectivity significance.

What Investors Are Underpricing

The infrastructure narrative is gaining traction. What is less well-articulated, and where the risk of miscalculation is highest, is the political and regulatory dimension that will ultimately determine which of these investments deliver their intended value.

Subsea cable infrastructure does not exist in a regulatory vacuum. Landing rights, coastal zone approvals, spectrum allocation, and interoperability with national telecommunications frameworks are all subject to domestic regulatory processes that vary significantly in their transparency, predictability, and susceptibility to political influence.

In several Southeast Asian markets, the gap between stated investment openness and operational reality remains substantial. The SJC2 experience, years of delay attributable to a single government's permit demands in contested waters, is a vivid illustration of how quickly political friction can transform a commercial timeline. Regulatory frameworks for digital infrastructure are in many cases nascent, inconsistently applied, or subject to revision as governments recalibrate their own strategic interests in the sector.

The involvement of US government bodies (through USTDA grants and FCC scrutiny) and the corresponding sensitivity of Chinese-linked operators to projects they are excluded from, means that cable investment is increasingly read by host governments through a geopolitical lens. That creates both opportunity and exposure for investors who have not adequately mapped the stakeholder landscape.

There is also a deeper question of institutional readiness. Connectivity infrastructure generates value only if the surrounding ecosystem, including data governance frameworks, cross-border data flow agreements, cloud regulation, and cybersecurity architecture, is capable of absorbing and enabling it. On this dimension, the gap between aspiration and capability varies considerably across the region.

Thailand has made meaningful progress: BOI incentives for data centres, a developing regulatory framework under the NBTC, and a geographic position that makes it a natural landing point for Indian Ocean routes. But progress is not uniformity, and the policy environment remains one where understanding how decisions are actually made, not just how they are formally structured, is a material advantage.

Thailand's evolving policy environment is itself in transition following the February 2026 election, the implications of which for investment and regulatory continuity we analysed here.

Resilience as a Strategic Lens

The broader implication of this shift extends beyond cable routes.

Resilience as an infrastructure principle reflects a fundamental reassessment of how risk is priced in long-horizon investment decisions. The efficiency paradigm optimised for cost and speed under an assumption of systemic stability. The resilience paradigm accepts that stability is not guaranteed and builds redundancy, diversification, and optionality into the investment itself.

This logic is already visible in semiconductor supply chains, in pharmaceutical manufacturing footprint decisions, and in the accelerating geographic diversification of data centre capacity. Subsea cables are the latest domain in which it is becoming structurally dominant.

For investors and multinationals operating across Asia-Pacific, the implication is not simply to track which cables are being built. It is to understand the strategic logic animating those decisions, the political economy shaping which projects advance and which stall, and the regulatory environments that will determine operational outcomes on the ground.

Infrastructure investment without that understanding is exposure, not strategy.

What This Means in Practice

The shift from efficiency to resilience is creating a new category of decision-making complexity, one that sits at the intersection of technology investment, regulatory navigation, and geopolitical positioning.

For digital infrastructure investors, the questions are no longer purely technical. They are questions about which markets have the institutional architecture to support long-term investment, which regulatory processes carry real risk, and which stakeholder relationships need to be in place before capital is committed.

For multinationals whose operations depend on digital connectivity (and in 2026, that is effectively all of them) the questions are about exposure and continuity: where are the vulnerabilities in current infrastructure dependencies, and how are those dependencies changing?

These are not questions that yield to standard due diligence. They require a different kind of engagement, one grounded in understanding how systems actually function, who shapes outcomes in practice, and where the pressure points are before they become problems.

The shift from efficiency to resilience is, at its core, a shift in how sophisticated investors think about risk. The cables being laid today are not just infrastructure. They are a map of how capital, governments, and great powers expect the next decade to unfold.

Reading that map accurately and positioning accordingly is what separates investors who navigate this environment from those who are simply exposed to it.

Google Cloud (24 November 2025). TalayLink Subsea Cable to Connect Australia and Thailand. cloud.google.com/blog/products/infrastructure/talaylink-subsea-cable-to-connect-australia-and-thailand

U.S. Trade and Development Agency (21 January 2026). USTDA Advances Trusted Submarine Cable Linking India and Southeast Asia. ustda.gov/ustda-advances-trusted-submarine-cable-linking-india-and-southeast-asia

NEC Corporation (19 December 2024). NEC Completes Construction of the Asia Direct Cable (ADC). nec.com/en/press/202412/global_20241219_02.html

Submarine Networks (January 2026). NTT Forms JV for the $1 Billion Intra-Asia Marine Cable Project. https://www.submarinenetworks.com/en/systems/intra-asia/i-am-cable/ntt-forms-jv-for-the-$1-billion-intra-asia-marine-cable-project

Submarine Networks (July 2025). SJC2 Subsea Cable is Finally Operational. https://www.submarinenetworks.com/en/systems/intra-asia/sjc2/sjc2-subsea-cable-is-operational

Telecom Review Asia (2024). The Asia Direct Cable System and Its Role in Shaping the Region's Digital Future. https://www.telecomreviewasia.com/news/featured-articles/4798-the-asia-direct-cable-system-and-its-role-in-shaping-the-region-s-digital-future/

Developing Telecoms (28 January 2026). Why a New India–Singapore Subsea Cable Matters for Indo-Pacific Connectivity. https://developingtelecoms.com/telecom-technology/optical-fixed-networks/19674-why-a-new-india-singapore-subsea-cable-matters-for-indo-pacific-connectivity.html

East Asia Forum (17 October 2025). Southeast Asia's Undersea Cables Under Great Power Pressure. https://eastasiaforum.org/2025/10/17/southeast-asias-undersea-cables-under-great-power-pressure/

ISEAS–Yusof Ishak Institute (14 March 2025). The Struggle for Subsea Cable Supremacy in Southeast Asia. ISEAS Perspective 2025/21. https://www.iseas.edu.sg/wp-content/uploads/2025/02/ISEAS_Perspective_2025_21.pdf

CSIS (November 2025). The Strategic Future of Subsea Cables: A Guidebook. https://csis-website-prod.s3.amazonaws.com/s3fs-public/2025-08/250826_Murphy_Subsea_Cables.pdf?VersionId=hwPU4f9ChRSiJmvEVVVDnOERpx3kCBYP